If you have been thinking about selling your home to a cash buyer, the first question that probably crosses your mind is a simple one: how much will they actually offer? The answer depends on who is buying, what your home looks like, and how fast you need to move. This guide breaks down the real numbers behind cash offers so you can walk into any conversation with a buyer knowing exactly what to expect and whether a deal is truly worth taking.

The short answer: Cash buyers typically pay between 70% and 90% of a home’s current market value. Investors and house flippers tend to offer on the lower end, around 60% to 75%. iBuyer platforms like Opendoor may offer closer to 88% to 97% before fees. Owner-occupant cash buyers tend to come in around 76% to 84%. The exact number shifts based on your home’s condition, your local market, and your timeline.

What Percentage of Market Value Do Cash Buyers Typically Offer?

Most cash buyers offer somewhere between 70% and 90% of what your home is currently worth on the open market. That range sounds wide, but it reflects real differences in who is buying and why.

A traditional real estate investor buying your home to flip it will aim for the lowest number in that range. Their business model depends on buying low, putting money into repairs, and reselling at a profit. They are not trying to lowball you out of spite. They are working a formula that only works if they have enough room between what they pay and what they eventually sell for.

Sellers who work with iBuyers see higher percentages on paper. Opendoor and Offerpad have reported offer ranges of 88% to 97% of market value. However, those platforms charge service fees that typically bring the net payout to around 92% or even lower depending on the property and market conditions.

If you are selling to someone who simply wants to live in your home and happens to be paying cash, you may see offers closer to 76% to 84% of the After-Repair Value (ARV). These buyers are not planning to renovate for profit, so they can afford to offer a bit more.

How the 70% Rule Works (And When It Actually Applies)

The 70% rule is the standard formula most real estate investors use to calculate their maximum offer. Understanding it helps you see where a low offer is coming from and whether it is reasonable given your home’s situation.

The Investor Formula Broken Down

The formula works like this: an investor will pay no more than 70% of a home’s After-Repair Value, minus the estimated cost of repairs needed. If your home would be worth $250,000 fully renovated, and it needs $30,000 in work, an investor using this formula would offer a maximum of $145,000.

That may feel low. But for an investor taking on carrying costs, renovation risk, and resale uncertainty, that margin is often what makes the deal viable at all. When they offer above that threshold, they are betting on a rising market or underestimating repair costs, both of which can quickly turn a project unprofitable.

Why ARV Matters More Than Asking Price

ARV stands for After-Repair Value, meaning what your home would sell for on the open market once it is in top condition. Cash buyers do not base their offers on your current listing price or what Zillow shows. They base it on what the home will be worth after they put money into it.

This is why two homes on the same street with the same square footage can receive very different cash offers. A home that needs a full kitchen renovation, new flooring, and a roof replacement carries a far heavier repair deduction than one that just needs a coat of paint and some landscaping. Understanding your own ARV before you speak with buyers puts you in a much stronger position to evaluate any offer you receive.

What Type of Cash Buyer Are You Dealing With?

Not every cash buyer operates the same way. The type of buyer reaching out to you changes the offer range, the timeline, and the overall experience significantly.

Real Estate Investors and House Flippers

These buyers represent the most common type of cash purchaser in the off-market space. They buy homes as-is, handle all repairs themselves after closing, and resell for profit. Their offers follow the 70% rule closely, and they move quickly. Some can close in as few as 7 to 14 days.

If speed and certainty matter more to you than squeezing every dollar out of the sale, an investor offer can genuinely make sense. You skip repairs, agent commissions, open houses, and the anxiety of a deal falling through because a buyer’s mortgage fell apart at the last minute.

iBuyers Like Opendoor and Offerpad

iBuyers use technology and automated valuation models to make fast offers at scale. Their headline percentages look better than what a traditional investor offers. But the math changes once you factor in their service fees, which typically run between 5% and 8%, along with repair deductions they calculate on their own after a home assessment.

iBuyers also tend to operate in specific markets and are more selective about the homes they buy. If your home needs significant work or sits outside their active service area, you may not qualify for an iBuyer offer at all.

Owner-Occupant Cash Buyers

Sometimes the buyer paying cash simply wants to live in the home. These are not investors. They could be someone who recently sold their own home, a retiree relocating, or a buyer who received an inheritance and wants to skip the mortgage process. Because they are not planning to renovate and resell, they have less need to account for repair costs in their calculation. This group tends to offer the closest number to full market value among cash buyers.

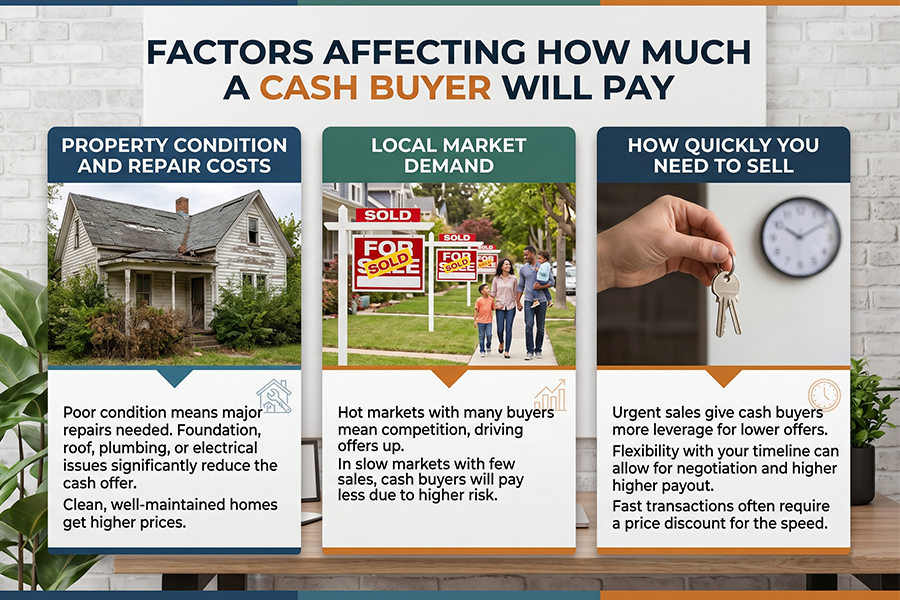

What Factors Affect How Much a Cash Buyer Will Pay?

Even within the ranges above, specific circumstances push an offer up or down. Knowing these variables helps you understand why two cash offers on similar homes can look very different.

Property Condition and Repair Costs

This is the biggest factor in any cash offer. A home that needs a new roof, outdated electrical work, foundation repairs, or major cosmetic updates will receive a lower offer than a home that is move-in ready. Every dollar an investor expects to spend in repairs comes directly out of what they can pay you at closing.

If your home is in decent shape and mainly needs cosmetic updates, you are in a better position than if structural or mechanical systems need replacement. Being honest with yourself about your home’s condition before you start talking to buyers will save you from feeling blindsided by a low offer later. You can also review our guide on what not to fix when selling a house to figure out where repairs are actually worth your time and money.

Local Market Demand

In markets where homes sell fast and inventory stays low, cash buyers will stretch their offers further to compete. In slower markets where homes sit for weeks or months, buyers have more leverage and tend to stick closer to the low end of their formula.

If you are in a competitive zip code, a cash offer at 80% of ARV may actually be less than you could get on the open market with the right agent. In a softer market, that same 80% offer starts to look much more appealing when you consider the time and carrying costs of a traditional listing.

How Quickly You Need to Sell

Urgency shifts the power dynamic in any negotiation. If you need to close in two weeks because of a job relocation, a financial situation, or a family change, a cash buyer knows that and may come in with a tighter offer. If you have flexibility on timing and can afford to wait for the right number, you have more room to counter or walk away.

This does not mean cash buyers are predatory. It means they are running a business with real constraints, just as you are navigating real circumstances. The best transactions happen when both sides are honest about what they need.

Is Selling for Cash Worth Less Money?

On paper, yes. A cash offer almost always comes in below what you could get listing your home with an agent in a healthy market. But the comparison is rarely that clean.

When you sell the traditional way, you typically spend 2% to 5% on agent commissions, another 1% to 3% on closing costs, and potentially thousands more on repairs, staging, and carrying costs while your home sits on the market. Some sellers also deal with deals falling through due to buyer financing issues, which pushes the timeline out further.

With a cash sale, you skip most of those costs. You also skip the uncertainty. According to Redfin, even cash transactions carry closing costs of roughly 1% to 3%, but sellers avoid the larger expenses that come with a financed sale.

Whether selling for cash is worth it comes down to your personal situation. If you are trying to sell your house fast due to a life change, a financial shift, or a property that needs more work than you can afford, the certainty and speed of a cash offer often outweigh the lower number on paper. If you have time, equity, and a home in good shape, the open market may serve you better.

How to Know If a Cash Offer Is Fair

A fair cash offer reflects your home’s actual condition and the real market around it. It is not necessarily the highest number you could get, but it should be a number that makes logical sense given the ARV, the repair costs, and the buyer’s risk.

Here are a few ways to check whether an offer holds up:

Start by getting a rough estimate of your home’s ARV. Look at recent comparable sales in your neighborhood for homes that are updated and move-in ready. That gives you the ceiling. Then honestly assess what repairs your home needs and what those repairs would cost. Subtract those costs from the ARV and multiply by 70% to 80%. That range is what a reasonable investor offer should land in.

If an offer falls well below that floor without a clear explanation, ask the buyer to walk you through their math. A reputable buyer will be transparent about how they arrived at their number. If they cannot explain it, that tells you something important.

You can also request multiple offers before you commit. Sisters Who Buy Houses provides a no-pressure, straightforward cash offer with zero obligation. You can see our process on our how it works page and get a cash offer today when you are ready.

Frequently Asked Questions

How much less do cash buyers pay for houses?

Cash buyers typically pay 10% to 30% below market value compared to financed buyers. The gap narrows with iBuyers and owner-occupant cash buyers and widens with investors who account for heavy repair costs. The actual difference in your case depends on your home’s condition, your local market, and the type of buyer making the offer.

Is it worth it to sell your home for cash?

Selling for cash is often worth it if you need to close fast, want to avoid repairs or showings, or are dealing with a property in poor condition. You receive less than market value but save on commissions, staging, and the risk of deals falling through. For many sellers, the certainty and speed more than make up for the price difference.

What is the 3 3 3 rule in real estate?

The 3 3 3 rule is a general guideline some investors use when evaluating rental properties. It suggests looking for properties where the monthly rent equals at least 3% of the purchase price, the home is purchased at roughly 30% below market value, and the area has at least 3% annual appreciation. It is less commonly applied to cash home purchase scenarios and more specific to buy-and-hold investing.

Can I afford a $300k house on a $50k salary?

This question applies to buyers, not sellers. As a general rule, most lenders look for a debt-to-income ratio below 43%, and a $300,000 home at current interest rates would typically require a salary in the range of $60,000 to $80,000 depending on your down payment and existing debt obligations. Cash buyers do not face this constraint, which is one reason cash offers close faster.

Do cash buyers always pay less than market value?

Not always. Owner-occupant cash buyers sometimes pay at or near full market value, particularly in competitive markets where buyers need to move fast to win a home. The below-market offers come primarily from investors and flippers who need a margin to cover renovation costs and resale risk.

What closing costs do cash buyers and sellers still pay?

Even in a cash transaction, closing costs exist. Sellers typically pay 1% to 3% in closing costs, which may include title fees, transfer taxes, and prorated property taxes. Buyers pay similar fees on their end. The major savings come from skipping lender-related fees, which can add another 1% to 2% in a financed deal.

How fast can a cash buyer actually close?

Most cash buyers can close in 7 to 21 days depending on title work and any negotiated timelines. Some buyers offer flexible closing dates if you need more time to move. This speed is one of the primary reasons sellers accept lower cash offers rather than waiting 30 to 60 days for a financed deal to clear underwriting.

The Bottom Line

Cash buyers pay less than what your home might fetch on the open market, and now you know exactly why. The 70% rule, repair deductions, ARV calculations, and buyer type all shape the final number. None of this is random, and none of it has to feel intimidating.

Knowing the math puts you in control. You can evaluate any offer that lands in your inbox against the real numbers behind it. And if your situation calls for a fast, honest, no-hassle sale, working with a cash buyer who explains their process clearly is worth more than chasing a higher number that takes months to materialize.

If you are curious what your home might bring as a cash sale, read through our frequently asked questions or contact us directly. We are here to give you real answers, not a sales pitch.