Receiving a foreclosure notice feels like the floor dropping out from under you. Your first instinct might be to assume the house is gone and there’s nothing you can do. But that assumption costs homeowners thousands of dollars every year, and it doesn’t have to cost you.

Yes, you can sell a house in foreclosure — and in most cases, selling is far better than letting the bank take it. The key is understanding your timeline, your options, and what steps to take before the clock runs out.

This guide covers exactly how selling a house in foreclosure works, when you can still do it, how much time you realistically have, and what your best options are depending on your situation.

Quick Answer: You can sell a house in foreclosure as long as the foreclosure auction (also called a sheriff’s sale) has not yet taken place and your lender agrees to the sale. The pre-foreclosure period — between your first missed payment and the auction date — is your window to act. The national average foreclosure timeline is 592 days, which gives most homeowners more time than they realize.

What Does “In Foreclosure” Actually Mean?

Before we talk about selling, it helps to understand where you are in the process. Foreclosure is not a single event — it’s a legal process with multiple stages, and your options change depending on which stage you’re in.

Stage 1: Missed Payments. You miss one or more mortgage payments. Your lender will typically send notices and attempt contact. This is the earliest and best time to act.

Stage 2: Notice of Default (NOD). After 90 to 120 days of missed payments, your lender files a Notice of Default with the county. This is the official start of the foreclosure process and becomes a public record.

Stage 3: Pre-Foreclosure. The period between the NOD and the foreclosure sale. This is your primary window to sell the house, negotiate with your lender, or explore other options.

Stage 4: Foreclosure Auction. The property goes to auction. Once the auction is completed and the sale is confirmed by the court (in judicial states), your ability to sell is effectively gone.

Stage 5: Real Estate Owned (REO). If no one buys the home at auction, the bank takes ownership. The house becomes bank-owned property, and you lose all equity.

Understanding which stage you’re in tells you exactly how much time you have.

Can You Sell a House in Foreclosure? The Direct Answer

Yes, selling a house in foreclosure is legal and possible — but your window closes the moment the auction is finalized. Up until that point, you remain the legal owner of the property, which means you have the right to sell it.

The practical reality is that most homeowners have more time than they think. According to ATTOM data, the national average foreclosure timeline runs about 592 days. Some states run far longer — Louisiana averaged over 3,400 days in Q4 2025, and Kansas averaged more than 1,500 days. Even in faster states, you typically have weeks or months after receiving a Notice of Default before an auction date is set.

That time is not wasted time. It’s your opportunity to sell your house fast before the bank forces the sale at auction — usually for far less than market value.

There is one important distinction to understand: once the foreclosure auction takes place, selling becomes extremely difficult. Some states have a “redemption period” after the auction where you can technically reclaim the property by paying off the debt in full, but selling within that window is rarely practical and not guaranteed.

The bottom line: If the auction has not happened, you can sell. The earlier you act, the more options you have.

How to Sell a House in Foreclosure: Step by Step

Selling a house in foreclosure is not the same as a standard home sale. There are additional parties involved, tighter timelines, and specific requirements from your lender. Here’s how the process works.

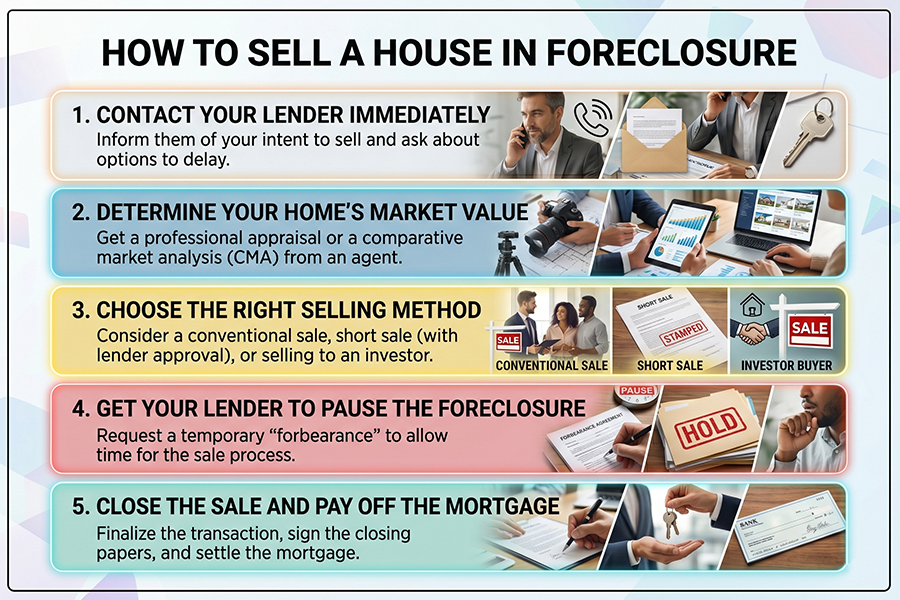

Step 1: Contact Your Lender Immediately

Your lender must be part of any sale that involves an outstanding mortgage. Call them as soon as you decide to sell. Be direct: tell them you want to sell the property to pay off the loan before the auction.

Most lenders will cooperate. Foreclosure is expensive for them too — the average lender loses significant money on a foreclosure auction compared to a pre-foreclosure sale. They have real financial motivation to work with you.

During this call, ask for the exact payoff amount on your mortgage, the current status of your foreclosure proceedings, whether a pending sale can pause or stop the foreclosure process, and what lender approval is required before you can close.

Step 2: Determine Your Home’s Market Value

Get a realistic picture of what your home is worth. You can request a free cash offer, ask a real estate agent for a comparative market analysis, or look at recent sales in your neighborhood.

This step matters because it determines whether you’re in a standard sale situation (home value exceeds your debt) or a short sale situation (home value is less than what you owe).

Step 3: Choose the Right Selling Method

There are three main paths for selling a house in foreclosure. Each has trade-offs.

Sell to a Cash Buyer or Investor

This is the fastest option and often the smartest choice when you’re facing a foreclosure timeline. Sisters Who Buy Houses and similar cash home buyers can close in days, not months — which matters enormously when an auction date is approaching.

Cash buyers don’t require you to make repairs, pass inspections, or stage the home. You sell as-is. The offer may be below retail value, but you walk away with cash in hand, your mortgage paid off, and no foreclosure on your record. For most homeowners in foreclosure, this trade-off is well worth it.

To see what your home could sell for in its current condition, you can get a cash offer today.

List with a Traditional Real Estate Agent

If you have enough time and your home is in decent shape, listing with an agent can get you closer to full market value. The challenge is timing. The traditional listing process — preparing the home, finding a buyer, negotiating, going through mortgage approval, and closing — typically takes 60 to 90 days. If your auction date is sooner than that, a traditional sale may not be realistic.

This option works best when you’re in the early stages of foreclosure, have 90+ days before your auction, and the home has genuine retail appeal.

Pursue a Short Sale

If your home is worth less than you owe on the mortgage, a traditional sale won’t fully pay off your debt. In that case, you may be eligible for a short sale — where your lender agrees to accept less than the full payoff amount in exchange for releasing the lien.

Short sales take lender approval, which adds time and uncertainty. Your lender can reject offers, change terms, or even push you into foreclosure while reviewing the short sale application. This isn’t the fastest or most reliable option, but it can be better than a foreclosure on your credit report in some situations.

Step 4: Get Your Lender to Pause the Foreclosure

Once you have a buyer or a serious offer in place, contact your lender again and request a foreclosure pause or forbearance to allow the sale to close. Many lenders will agree, especially if the sale will fully pay off the loan.

Get this agreement in writing. Do not assume a verbal commitment will hold.

Step 5: Close the Sale and Pay Off the Mortgage

At closing, the proceeds from the sale go first to pay off your outstanding mortgage balance, then to any other liens on the property (like a second mortgage or tax liens), and then any remaining equity goes to you.

If you work with an experienced title company or real estate attorney, they will handle the lender payoff coordination. Don’t skip this step — a clean title is essential for the buyer and to fully end the foreclosure process.

What Happens If You Don’t Sell Before Foreclosure?

Letting the foreclosure proceed without selling has serious, long-term consequences.

Credit damage. A completed foreclosure stays on your credit report for seven years and causes a significant drop in your credit score — often 100 to 150 points or more. This affects your ability to get a new mortgage, a car loan, or even rent an apartment.

Waiting period for a new mortgage. After a foreclosure, most lenders require you to wait three to seven years before qualifying for a new home loan. FHA loans require a minimum three-year wait; conventional loans typically require seven years.

Loss of equity. Foreclosure auctions routinely sell homes for well below market value. If you had any equity in your home, a foreclosure sale often wipes it out entirely. A pre-foreclosure sale, even at a slight discount, usually puts more money in your pocket than letting the bank handle it.

Deficiency judgment risk. In some states, if the foreclosure auction proceeds don’t cover your full mortgage balance, your lender can pursue a deficiency judgment against you for the difference. That means owing money even after losing the home.

Selling a House in Foreclosure: What About Repairs?

One concern that stops homeowners from selling is the condition of the home. When you’ve been struggling financially, keeping up with maintenance and repairs often takes a back seat. You may worry no buyer will want the house as-is.

Here’s what most homeowners don’t realize: you do not need to fix anything to sell a house in foreclosure. Cash buyers and real estate investors purchase homes in any condition — damaged roofs, outdated kitchens, foundation issues, structural problems, all of it.

You can check out our guide on what not to fix when selling a house to understand exactly which repairs are worth making and which ones you can safely skip — even in a traditional sale.

When the timeline is tight, selling as-is to a cash buyer removes all of the repair burden and most of the closing friction.

How Fast Can You Close When Selling a House in Foreclosure?

Speed is everything in a foreclosure sale. Here’s a realistic look at timelines by method.

Cash buyer / investor: 7 to 14 days. Sometimes faster if paperwork is straightforward. This is the most realistic option when you have an auction date approaching.

Traditional real estate listing: 60 to 90 days minimum. This can stretch longer in slower markets or if the home needs work to attract buyers.

Short sale: 90 to 180+ days. Short sales require lender approval, which adds weeks or months to the process and comes with no guarantee of success.

If you’re working against an auction date, a cash buyer is almost always the right call. Learn how the process works so you know exactly what to expect from start to finish.

Can You Sell a House That Is in Foreclosure if You Have a Second Mortgage?

Yes, but it adds complexity. A second mortgage is a separate lien on the property, and it must also be paid off at closing or settled before the sale can complete.

If your home’s value covers both mortgages, this is straightforward — the closing handles both payoffs simultaneously. If the home’s value doesn’t cover both, you’ll need to negotiate with one or both lenders about accepting less than the full amount owed. This is similar to a short sale situation and requires lender cooperation.

Don’t let a second mortgage stop you from exploring a sale. A cash buyer with experience in foreclosure situations will know how to navigate this. Contact us through our frequently asked questions page or reach out directly to talk through your specific situation.

Frequently Asked Questions

Can you sell a house when it is in foreclosure without lender approval?

If your home’s value fully covers the mortgage payoff, you don’t technically need separate lender approval — the payoff happens automatically at closing. However, if the sale price won’t fully cover what you owe, you need lender approval for a short sale. Either way, notifying your lender before you sell is strongly recommended.

Can you sell a house in foreclosure for cash?

Yes, and this is often the best option. Cash buyers can close quickly without the financing contingencies that slow down traditional sales. When you’re facing an auction date, a fast cash close is often the only realistic path.

Will selling stop the foreclosure?

Yes, once the sale closes and the mortgage is paid off, the foreclosure process ends. Your lender has no reason to continue the foreclosure if the debt is satisfied. Make sure your lender formally acknowledges this in writing before or at closing.

Does selling in foreclosure hurt your credit?

Less than a completed foreclosure does. A foreclosure stays on your credit for seven years and causes severe damage. A pre-foreclosure sale, even a short sale, is typically less damaging than a completed foreclosure — though it will still show on your report. A clean sale (where the full payoff is covered) has minimal credit impact beyond the missed payments already recorded.

Can I sell my house if I’m behind on payments but haven’t received a Notice of Default?

Absolutely, and this is the best time to sell. You have the most time, the most flexibility, and the most options. Don’t wait for a formal foreclosure notice to start exploring a sale.

What if I owe more than my home is worth?

This is a short sale situation. You’ll need to negotiate with your lender to accept less than the full balance owed. Many lenders agree to this because they’d rather receive a partial payoff than deal with a foreclosure auction. A real estate attorney can help you navigate the negotiation.

Can I stay in my home while it’s being sold in foreclosure?

Yes. Until the sale closes, you remain the legal owner and have the right to occupy the property. Some cash buyers also offer a leaseback option, allowing you to continue renting the home after the sale closes if you need additional time to relocate.

The Bottom Line: Act Quickly, But Don’t Panic

Selling a house in foreclosure is legal, possible, and often the smartest financial move you can make. The homeowners who come out of foreclosure with the least damage are the ones who act early, understand their options, and make a decision instead of waiting.

You have more time than you think, but that window doesn’t stay open forever. The closer you get to an auction date, the fewer options you have and the harder it is to sell on your terms.

If you’re facing foreclosure and want to understand your options without pressure, contact Sisters Who Buy Houses today. We buy houses in any condition, on your timeline, and we can give you a cash offer within 24 hours. No repairs, no agent fees, no uncertainty.

Your situation isn’t hopeless. Let’s talk.